Building a life is a lot like building a home; you need a solid foundation, and when you are planning for your later years, that foundation is built on where your money goes. Many buyers want to know if their hard-earned savings will stay in their pockets or disappear into the state treasury. Today, we are looking at the math behind your future, specifically the Tennessee vs North Carolina retirement tax comparison for 2026.

For the women leading their households or planning a legacy for their families, this choice is about more than just a lower bill. It is about security. It is about knowing that the house you build today will not become a financial burden tomorrow because of a shifting retirement tax landscape. We are going to examine why the Volunteer State and the Tar Heel State offer such different paths for your golden years.

State Income Tax: The Great Divide

This is where the foundation of your retirement plan either stays solid or starts to show some cracks. In my world of home building, “The Great Divide” is the perfect name for it because Tennessee and North Carolina are on completely opposite sides of the fence when it comes to taxing your income.

When we talk about a Tennessee vs North Carolina retirement tax comparison, we are looking at two states that have spent the last few years moving in different directions. Tennessee has doubled down on being a tax haven, while North Carolina has been trying to simplify and lower its rates, but they are starting from a very different place.

The Tennessee Model: Pure Simplicity

In Tennessee, our approach to retirement tax is as straightforward as a well-built rancher. We do not have a state income tax. Period.

For a long time, we had a small exception called the Hall Tax. This was a tax that hit seniors specifically because it taxed interest from savings and dividends from stocks. If you had spent your life being frugal and investing for the future, the state took a piece of that growth. But as of 2021, that tax was completely wiped off the books.

Now, in 2026, the Volunteer State is as pure as it gets. Whether you are earning a paycheck from a part-time job at the local hardware store or pulling $10,000 a month from a massive 401(k), the state of Tennessee does not ask for a single penny of it. For many of my clients, this is the “brilliant” part of the move. It removes an entire layer of bureaucracy and cost from their lives. You don’t have to keep track of state tax brackets or worry about a “tax cliff” if you earn a little more one year.

The North Carolina Model: The Flat Tax Path

North Carolina has taken a different route. They used to have a complex system with different brackets, but they have moved to what we call a “flat tax.” This means every person pays the same percentage, regardless of whether they make $30,000 or $300,000.

As of January 1, 2026, the North Carolina income tax rate has dropped to 3.99%. Now, to be fair, the folks in Raleigh have done a lot of work to bring that number down from where it used to be (it was over 5% just a few years ago).

But here is where the divide really opens up. While 3.99% sounds small, it is a retirement tax on almost everything. Unless your money is coming from Social Security, which both states leave alone, North Carolina is going to take nearly 4 cents of every dollar you “earn” in retirement.

Breaking Down the Math

Let’s look at this with the precision I use when estimating a lumber load. If you are a married couple in Johnson City with $100,000 in taxable retirement income:

Tennessee State Tax: $0

North Carolina State Tax: Approximately $3,990

That $3,990 isn’t just a number on a page. In the Tri-Cities, that covers your homeowners insurance, your water bill, and probably your electricity for the entire year. By choosing to stay on the Tennessee side of the line, you are effectively getting your utilities paid for by the state’s tax policy.

The Female Perspective on Financial Security

We often find that the women we work with are the ones most concerned about this “Great Divide.” They are looking at the long-term sustainability of the household. If one spouse passes away, the survivor is often left with a smaller income but many of the same expenses.

In North Carolina, that survivor still has to factor in that 3.99% retirement tax on their remaining pension or IRA withdrawals. In Tennessee, that burden simply doesn’t exist. It provides a level of financial “insulation” that protects you against future tax hikes. Once a state doesn’t have an income tax, it is politically very difficult to start one. In a state that already has one, like North Carolina, the rate can go up just as easily as it went down.

Why It Matters for Your Custom Build

As your Home Building Experts, we see how this divide affects the homes we build. When people move from North Carolina to Tennessee, they often take that tax savings and put it directly into the “bones” of their home. They might choose 2×6 construction for better insulation or upgrade to high-efficiency windows.

They are trading a “forever tax” to the state for a one-time investment in a home that will save them even more money on energy bills later. That is what I call a precise, high-integrity move.

Retirement Income: Social Security, 401(k)s, and Pensions

Now, let’s look at the specific types of money you will be living on. Most people think all retirement money is treated the same, but that is not the case. Your retirement tax bill depends heavily on where your money comes from.

First, the good news: both Tennessee and North Carolina are very friendly when it comes to Social Security. Neither state taxes your Social Security benefits. This is a huge win for everyone. However, things change when we look at your 401(k), IRA, or private pension.

In Tennessee, these withdrawals are completely tax-free at the state level. Because we have no income tax, the state does not care if you take out $2,000 or $20,000 a month. This makes Tennessee one of the most attractive places in the country for people with large retirement accounts. If you have been diligent about saving in your 401(k) for thirty years, Tennessee rewards that diligence by letting you keep the whole pie.

In North Carolina, your 401(k) and IRA withdrawals are taxed at that 3.99% flat rate. While it is a fair system in that everyone pays the same percentage, it is still a retirement tax that you have to account for. If you are used to living in a state with high taxes, 3.99% might seem like a bargain, but compared to Tennessee’s 0%, it is a cost you need to consider.

Pensions are handled similarly. Tennessee does not tax them. North Carolina does, with one major exception. There is something called the “Bailey Settlement.” This applies to people who were “vested” in certain government retirement systems (like federal, state, or local NC government plans) by August 12, 1989. If you fall into that group, your pension might be exempt from North Carolina state tax. But for most private-sector workers moving into the area, your pension will likely be subject to the state’s flat tax.

For the women who are managing the family legacy, this difference is vital. If you are the one making sure the bills are paid and the savings are growing, that 3.99% difference can change how you plan for long-term care or family inheritances. A lower retirement tax burden means more flexibility for the “what-ifs” in life.

Property Taxes: Protecting Your Home Investment

Now we look at property taxes. They are the “forever bill” of homeownership. Even after you pay off your mortgage, you still have to pay the tax man. When you are comparing Tennessee and North Carolina, you have to look at the effective tax rates.

Tennessee has some of the lowest property taxes in the United States. Our effective rate is often around 0.45% to 0.50%. For a home worth $400,000, your annual tax might be around $2,000. In the Tri-Cities, we also have several programs designed to help seniors stay in their homes.

One of these is the Property Tax Freeze. If you are 65 or older and meet certain income limits, the state can “freeze” the amount of tax you pay on your primary residence. Even if your home value goes up or the tax rate increases, your bill stays the same. There is also a Property Tax Relief program that provides a rebate to low-income seniors and disabled veterans. This is a core value of ours in Tennessee: we want to make sure the people who built our communities can afford to stay in them.

North Carolina’s property taxes are also relatively low compared to the national average, but they are typically higher than Tennessee’s. You can expect an effective rate between 0.70% and 0.85% in many counties. On that same $400,000 home, your tax bill might be closer to $3,200. North Carolina does offer a “Homestead Exclusion” for seniors. This program can exclude $25,000 or 50% of your home’s value (whichever is greater) from your taxable amount if you meet the income requirements.

However, the “brilliance” of Tennessee’s approach is that our base rates are already so low that many people do not even need an exclusion to feel comfortable. When designing a home for a couple in their 60s, we talk about “right-sizing.” We want a home that is efficient and easy to maintain. Having a low property retirement tax bill is a major part of that efficiency. It means you can spend your money on high-quality materials and finishes rather than sending it to the county office.

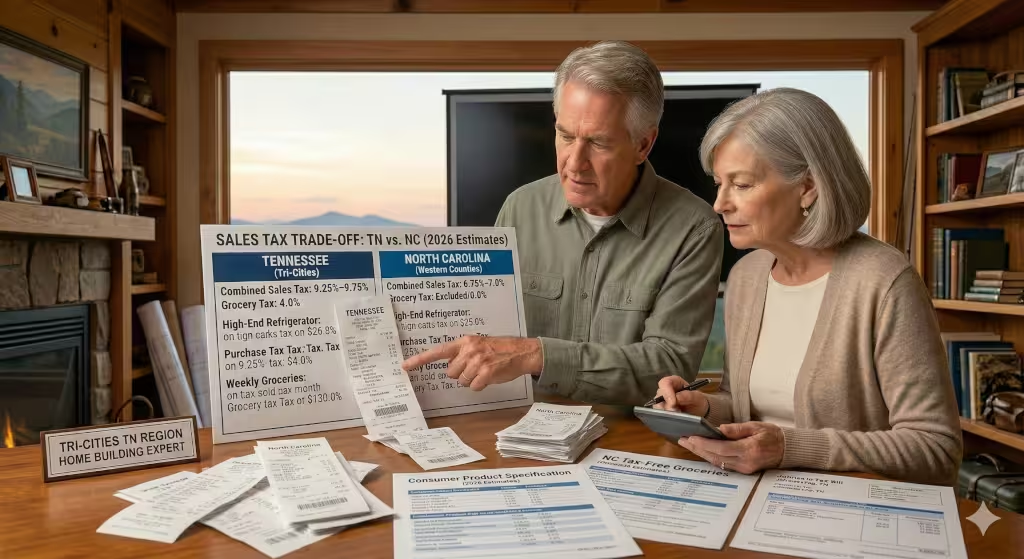

The Sales Tax Trade-off

Now, we have to be direct with you because integrity is one of my core values. Tennessee does not have an income tax, but the money has to come from somewhere. That “somewhere” is the sales tax.

Tennessee has one of the highest sales tax rates in the country. The state rate is 7%, and local governments can add up to 2.75% on top of that. In the Tri-Cities, you are looking at a total of 9.25% to 9.75% on most things you buy. This includes groceries, though the state does tax groceries at a lower rate of about 4%. If you are a big spender who loves to buy new cars, expensive clothes, and high-end furniture, you will feel this tax.

North Carolina has a much lower sales tax. Their total rate usually hovers around 6.75% to 7%. They also have a lower tax on groceries. If you spend a large portion of your income on physical goods, North Carolina’s lower sales tax might balance out its income tax.

This is where the “precision” of your planning comes in. You have to look at your own spending habits. If you have a high income but live a very modest life, Tennessee is almost certainly the better financial choice. If you have a modest income but spend a lot on taxable goods, the gap between the two states narrows.

Most retirees find that the savings from having zero income tax in Tennessee far outweigh the extra 2% or 3% they pay at the cash register. Think about it this way: your 401(k) withdrawals might be $60,000 a year. In NC, that is $2,400 in tax. To pay $2,400 in extra sales tax in TN (assuming a 2.5% difference), you would have to spend nearly $100,000 on taxable goods. Most people simply do not spend that much on “stuff” in retirement.

Common Questions Answered about Retirement Tax between NC and TN

People often ask about the “hidden” costs of moving between these states. Here are a few common queries I get at the job site.

Which state has better healthcare for retirees?

This is a common question. North Carolina is famous for its medical centers, especially around Durham and Winston-Salem. However, the Tri-Cities area in Tennessee has a very strong healthcare network centered around the Ballad Health system and the Quillen College of Medicine. For most routine care and even specialized needs, both states are excellent.

Is Tennessee a “tax haven” for retirees?

Yes, it is often ranked in the top five most tax-friendly states for retirement. Because of the 0% income tax and no inheritance tax, it is very hard to beat.

Does North Carolina tax out-of-state pensions?

Yes. If you worked in New York or Ohio and move to North Carolina, your pension will be taxed at the state’s flat rate. Tennessee will not touch it.

What is the 2026 federal senior deduction?

This is a new piece of information that is making a big difference. In 2026, many seniors are benefiting from a new federal deduction that can eliminate federal income tax on Social Security for many middle-income households. This makes the state-level retirement tax even more important, as it might be the only income tax you have left to pay.

Making Your Choice

Choosing between Tennessee and North Carolina for your retirement is about more than just the mountains and the lakes. It is a technical decision that requires precision and integrity in your planning.

If you value keeping every dollar of your retirement account and having some of the lowest property taxes in the nation, Tennessee is likely your winner. If you prefer a lower sales tax and do not mind a small, flat income tax, North Carolina offers a beautiful alternative.

Many more people are choosing Tennessee because it offers a “clearer” financial future. You know where you stand when the state rate is zero. It allows us to build better homes because our clients have more predictable budgets.

We hope this guide has helped you understand the nuances of the retirement tax in our region. Whether you decide to build with me in the Tri-Cities or head over the mountain into the Carolinas, make sure you are doing the math for your specific situation.

A Comparison of the Taxes between Asheville, NC and Johnson City, TN

We have put together a breakdown that highlights the financial reality of choosing between these two locations. We deal in blueprints and spreadsheets every day, and find that seeing the numbers side-by-side helps cut through the noise.

In this scenario, we are looking at a retiree with an $80,000 annual income from a 401(k) or pension, living in a $450,000 home, and spending about $30,000 a year on taxable goods.

2026 Retirement Tax Comparison: Johnson City vs. Asheville

| Tax Category | Johnson City, TN | Asheville, NC |

| Estimated Annual Income (401k/Pension) | $80,000 | $80,000 |

| State Income Tax Rate (2026) | 0.00% | 3.99% |

| State Income Tax Owed | $0 | $3,192 |

| Social Security Tax | $0 | $0 |

| Estimated Home Value | $450,000 | $450,000 |

| Avg. Property Tax Rate | ~0.46% | ~0.75% |

| Annual Property Tax Owed | $2,070 | $3,375 |

| Estimated Annual Taxable Spending | $30,000 | $30,000 |

| Avg. Combined Sales Tax Rate | 9.50% | 7.00% |

| Annual Sales Tax Paid | $2,850 | $2,100 |

| Total Estimated Annual State Tax | **$4,920** | $8,667 |

The Precision Analysis

When you look at the total estimated state tax, you can see a difference of $3,747 per year. In the world of home building, that is the equivalent of a high-end appliance package or a significant upgrade to your landscaping, every single year.

The Income Tax Factor: This is the heaviest hitter. Because North Carolina applies a flat tax to your 401(k) withdrawals, you are starting $3,192 behind Tennessee before you even leave the house.

The Property Tax Factor: While both states are reasonable compared to the Northeast or West Coast, Tennessee’s lower rates keep an extra $1,305 in your pocket annually in this specific scenario.

The Sales Tax Factor: Here is where North Carolina gains a bit of ground. You would save about $750 a year at the register in Asheville. However, as you can see, that savings doesn’t come close to making up for the income and property tax differences.

This comparison shows why so many people are choosing the Tennessee side of the border. It allows for a more competent and predictable long-term financial plan.